As you prepare your tax filings in 2023, it’s worth noting that there are a few updates to keep in mind for this year. Among these changes are an increased standard deduction, adjusted tax brackets, and modifications to certain tax credits and deductions. But before we dive into the details, here are the important tax filing dates for 2023.

Important Tax Filing Dates for 2023

- April 18, 2023, is the tax filing deadline for all federal, Massachusetts, and Rhode Island tax returns and payments.

- October 16, 2023, is the deadline if you request an extension for federal and Massachusetts / Rhode Island tax filings.

Tax Year vs. Tax Season

Before we go any further, let’s explain the difference between two common phrases you will often hear: tax year and tax season. These are distinct and not interchangeable.

- Tax Year: The tax year is the actual year where you earn income, pay income taxes, make charitable contributions, work side gigs, etc.

- Tax Season: The tax season is when you file, report, and pay any taxes owed from the last year.

- 2023 Tax Season for the 2022 Tax Year: During the 2023 tax season, you are filing taxes for the 2022 tax year.

When Can You File Your Taxes in 2023?

Tax season for 2023 begins in late January. During this time most income filers receive a W-2 form from your employer, even if you own a business that pays you a salary. Additionally, if you’re a freelancer, you should keep an eye out for 1099 forms from each of your clients.

Income Tax Forms for Tax Year 2022

Here is a list of possible documents you will need to collect and file to show your taxable income for 2023. Not all forms are necessary if they do not apply to your income situation for 2022.

- Income from jobs: forms W-2 for you and your spouse

- Investment income—various forms 1099 (-INT, -DIV, -B, etc.), K-1s, stock option information

- Income from state and local income tax refunds and/or unemployment: forms 1099-G

- Taxable alimony received

- Business or farming income—profit/loss statement, capital equipment information

- If you use your home for business—home size, office size, home expenses, office expenses.

- IRA/pension distributions—forms 1099-R

- Rental property income/expense—profit/loss statement, rental property suspended loss information

- Social Security benefits—forms SSA-1099

- Income from sales of property—original cost and cost of improvements, escrow closing statement, canceled debt information (Form 1099-C)

- Prior year installment sale information—Forms 6252, principal and Interest collected during the year, SSN and address of payer

- Other miscellaneous income—jury duty, gambling winnings, Medical Savings Account (MSA), scholarships, etc.

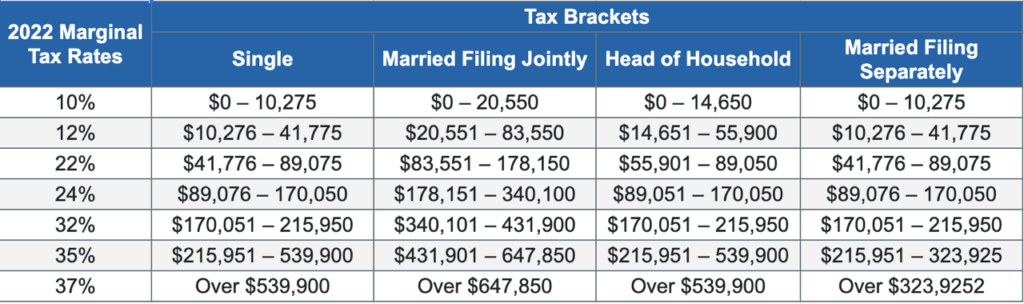

Federal Income Brackets and Rates for Tax Year 2022

Your tax rate (the percentage of your income you pay in taxes) is based on what tax bracket (income range) you’re in.

For example, if you’re single and your income for 2022 was $75,000, then you’re in the 22% tax bracket. But that doesn’t mean your tax rate is a flat 22%. Instead, part of your income is taxed at 10%, another part at 12%, and the last part at 22%. The tax brackets went up a few hundred dollars to account for inflation in 2022 (please reference the chart below). Remember, for 2023 you are filing taxes on your 2022 income.

2022 Marginal Income Tax Rates and Brackets

Massachusetts Income Tax Rate for Tax Year 2022

The state of Massachusetts has a flat rate personal income tax rate. Massachusetts’s individual income tax rate is fixed at 5.00% for all filing status tax returns.

Rhode Island Income Tax Rate for Tax Year 2022

- Tax rate of 3.75% on the first $68,200 of taxable income.

- Tax rate of 4.75% on taxable income between $68,201 and $155,050.

- Tax rate of 5.99% on taxable income over $155,050.

The Single, Married Filing Jointly, Married Filing Separately, and Head of Household income tax bracket amounts are all the same for the state of Rhode Island.

Lowering Your Taxable Income With Deductions and Credits

When it comes to filing taxes, deductions and credits can help to reduce your overall tax liability. There are several types of deductions that you may be eligible for, such as a standard deduction or itemized deductions. The standard deduction is a fixed amount that can be claimed by taxpayers who do not itemize their deductions, while itemized deductions allow you to deduct specific expenses, such as charitable contributions, mortgage interest, and state and local taxes.

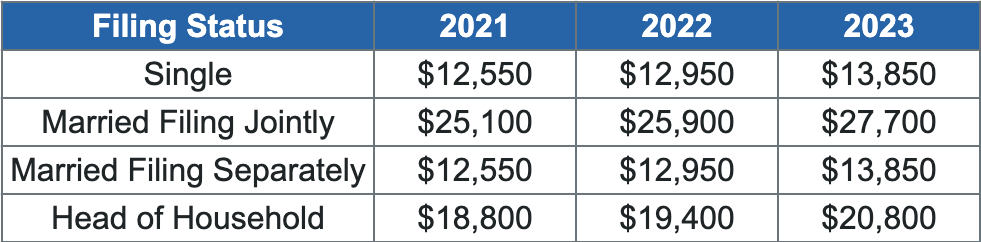

Standard Deductions are Higher in 2022 and 2023

For tax years 2022 and 2023, the standard deduction went up to adjust for inflation.

Tax Deductions and Credits to Consider for Tax Season 2023

The government offers a number of deductions and credits to help lower your tax burden. Here is a brief overview of how both work.

Tax deductions help lower the amount of your income that can actually be taxed. Some deductions are only available if you itemize your deductions, while others are still available even if you decide to take the standard deduction.

Tax credits are dollar amounts actually subtracted from your tax bill, and there are two types: refundable and nonrefundable. If a credit is greater than the amount you owe and it’s a refundable credit, the difference is paid to you as a refund. If it’s a nonrefundable credit, your tax bill will be reduced to zero, but you won’t get a refund.

Here are some itemized deductions and credits you might be able to claim on your 2022 tax return.

Charitable Deductions

You can deduct qualified charitable donations you made in 2022—as long as you itemize your deductions. The limit for this is 60% of your adjusted gross income (AGI), which is your total income minus other deductions you’ve already taken.

Medical Deductions

You can deduct any medical expenses above 7.5% of your adjusted gross income (AGI). For example, if your AGI was $100,000, you can deduct out-of-pocket medical expenses above $7,500 in 2022 or 2023. But you have to itemize your deductions in order to write off those expenses on your tax return.

Business Deductions

If you’re self-employed, there are a bunch of deductions you can claim on your tax return—including travel expenses and the home office deduction if you use part of your home for business purposes. Here is a list of business deductions for 2023.

Mortgage Interest Deductions

The mortgage interest deduction is a tax incentive for homeowners. This itemized deduction allows homeowners to subtract mortgage interest from their taxable income, lowering the amount of taxes they owe. In general, you can deduct the mortgage interest you paid during the tax year on the first $750,000 ($375,000 if married filing separately) of your mortgage debt for your primary home or a second home.

Child Tax Credit

The child tax credit (CTC) lets you credit up to $2,000 per dependent child under the age of 17. The income limit is $400,000 for married filing jointly and $200,000 for all the others. The CTC is also partially refundable up to $1,500.

Child and Dependent Care Credit

The child and dependent care credit is a nonrefundable credit that allows taxpayers to offset some of the costs of paying for services like babysitters, day care and in-home caregivers for older dependents.

You can claim 20–35% of up to $3,000 ($6,000 for two or more dependents) for the cost of care. The percentage of the credit depends on your AGI. Families with an AGI of $15,000 or less can claim the full 35%. As you earn more income, the credit is reduced. But a family with an AGI of over $43,000 can still claim the minimum credit rate of 20%.

Education Credits

The American opportunity tax credit (AOTC) is a partially refundable credit that pays for education expenses for students in the first four years of college. You can claim up to $2,500 per student—and if the credit brings your tax bill to zero, 40% (up to $1,000) will be refunded to you.

Another education credit is the lifetime learning credit (LLC). This one isn’t refundable, but it covers up to $2,000 in qualified educational expenses per return. While you can only take advantage of the AOTC for undergrad expenses, you can reap the benefits of the LLC for expenses related to all kinds of educational opportunities—from degree programs to technical classes to improving job skills.

You can actually claim both the AOTC and the LLC on your tax return—but not for the same student or the same expenses.

1099-K Changes Delayed Until 2023 Tax Year

The IRS was set to change the 1099-K form for this tax season, but those changes have just been delayed until the 2024 tax season. That’s good news for small business owners.

When you file your taxes in early 2023, a 1099-K form is only required if you’ve had more than 200 third-party business transactions a year and they’ve added up to more than $20,000 of income. These are the same thresholds for 1099-K forms as in previous years.

Smaller Tax Refunds for 2023

The IRS warned people to expect smaller tax refunds in 2023 based on two reasons:

- There were no economic impact payments in 2022, so taxpayers won’t get an extra stimulus payment in their 2023 tax refund checks.

- Expanded tax credits and deductions—like the child tax credit and charitable contributions deduction—reverted to their pre-COVID-19 amounts.

Filing Your Taxes in 2023

Preparing for tax season may feel like a daunting task, but being organized and informed can make the process smoother and less stressful. Make sure to gather all the necessary documents, such as W-2 and 1099 forms, and any records of your income and expenses mentioned above. Additionally, talk to your accountant/tax preparer about the available tax deductions and credits to help lower your tax bill. With the right preparation and support from your bookkeeper and tax professional, you can navigate the 2023 tax season with ease and confidence.